-

Nineteen states and three major cities now have them. Cheap and easy usually isn't best.

June 22 Bookkeeper360

Bookkeeper360 -

With about 41 million American workers lacking access to a retirement plan through their jobs, experts say advisors could play a pivotal role.

May 4

May 4

-

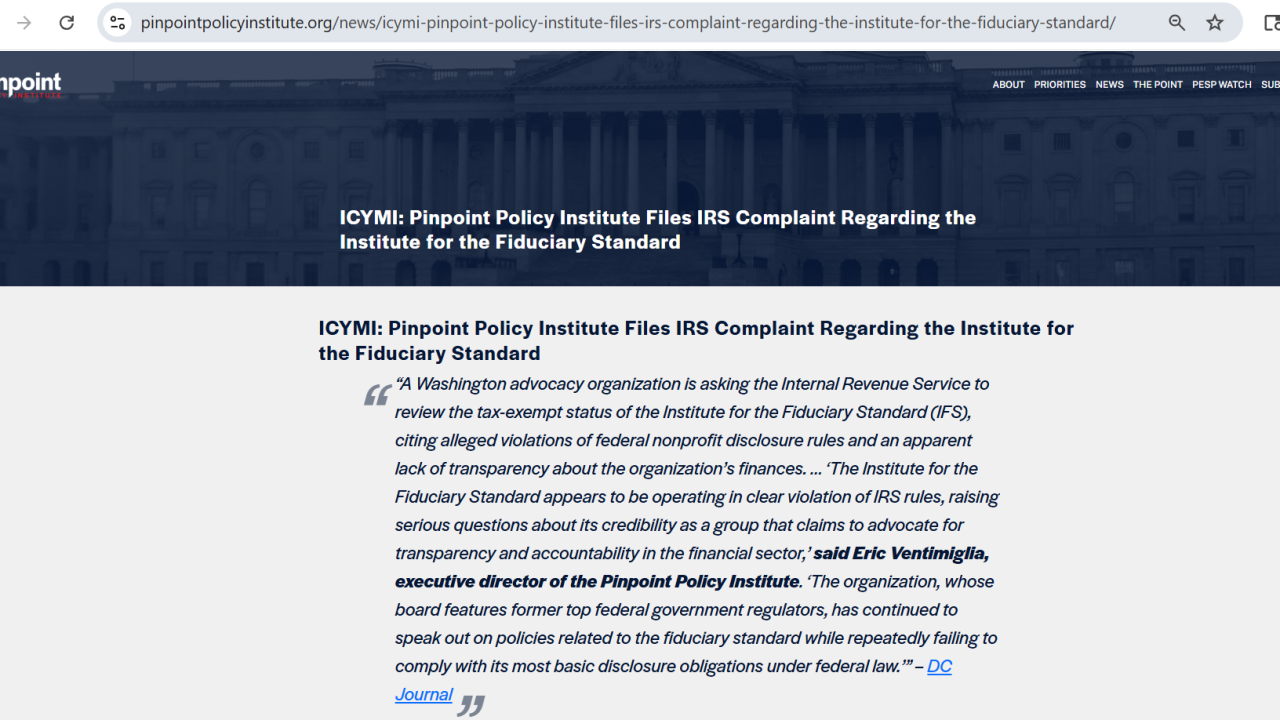

The Pinpoint Policy Institute's public campaign against the Institute for the Fiduciary Standard reflects a mysterious phase of the ongoing debate on private investments in 401(k) plans.

March 2

-

The president praised the impact of the One Big Beautiful Bill Act and his tariffs despite a Supreme Court ruling, while proposing new investment accounts.

February 25

February 25

-

The Internal Revenue Service increased the annual retirement plan contribution limits for 2026 thanks to cost-of-living adjustments for inflation.

November 13

-

The industry asked for and received a delay in the rule from the IRS in 2023. Now that it's going into effect, here are the key implications for sponsors and savers.

November 11

-

The industry asked for and received a delay in the rule from the IRS in 2023. Now that it's going into effect, here are the key implications for sponsors and savers.

November 10

-

Responding — or not — to jurisdictions' notices; pitfalls of growth; e-invoicing; and other highlights from our favorite tax bloggers.

October 29

-

The institute is asking the Treasury and the Internal Revenue Service for greater clarity in their proposed regulations for the SECURE 2.0 Act of 2022.

March 25

-

Financial advisors and other industry professionals will be integral in boosting those generations' nest eggs by double digits through a Secure 2.0 provision.

February 26

-

The proposed regulations involve provisions of the SECURE 2.0 Act, including auto enrollment in 401(k) and 403(b) plans, and the Roth IRA catchup rule.

January 10

-

The SECURE 2.0 Act contained changes to traditional and Roth individual retirement accounts and 401(k) plans that are being phased in over several years.

December 24

-

The IRS introduced changes to certain contribution limits to 401(k) and retirement plans for 2025, while some limits will remain the same.

November 27 -

The adjustments reflect how inflation is slowing down and upcoming changes to the rules based on the Secure 2.0 Act and the Tax Cuts and Jobs Act.

November 4

-

The amount individuals can contribute to 401(k)s in 2025 has increased by $500 to $23,500, but the IRA limit remains $7,000.

November 1

-

Many plan participants told the U.S. Government Accountability Office they didn't understand their four main options — or the potential tax consequences.

June 24

-

The IRS and Labor Department issued guidance on the new savings vehicles, but financial advisors and other wealth management professionals have questions.

January 22

-

Retirement plan sponsors and advisers receive guidance from the IRS on how to legally incentivize plan participation.

January 18

-

Retirement plan sponsors and their financial advisors receive guidance from the IRS on how the Secure 2.0 Act opened the door for "de minimis financial incentives."

January 16 -

The big AI question; staff pay; sourcing nonresident income; and other highlights from our favorite tax bloggers.

November 14